May 13, 2026

Automating Hail Damage Assessment: From Field Uncertainty to Data-Driven Decisions

Hail damage in agriculture represents a recurring financial risk for both farmers and insurers. The challenge lies not only in the damage itself, but in its verification: did hail actually occur, and what is the true extent of the loss? When these questions cannot be answered with confidence, uncertainty emerges across claims handling and risk assessment.

As extreme weather events become more frequent and localized, the need for objective and scalable assessment methods is becoming increasingly urgent.

A process shaped by uncertainty

Traditional approaches to hail damage assessment are largely manual. They typically rely on field inspections conducted shortly after an event, where a limited number of samples form the basis for evaluating both the presence of damage and its severity.

This approach comes with inherent limitations. A small set of observations rarely captures the variability across an entire field. Timing also plays a critical role, as early inspections may not reflect a crop’s ability to recover. In addition, outcomes can vary between assessors, making consistency difficult to achieve.

For insurers, this often translates into longer processing times and a less robust foundation for decision-making.

A data-driven approach to hail verification

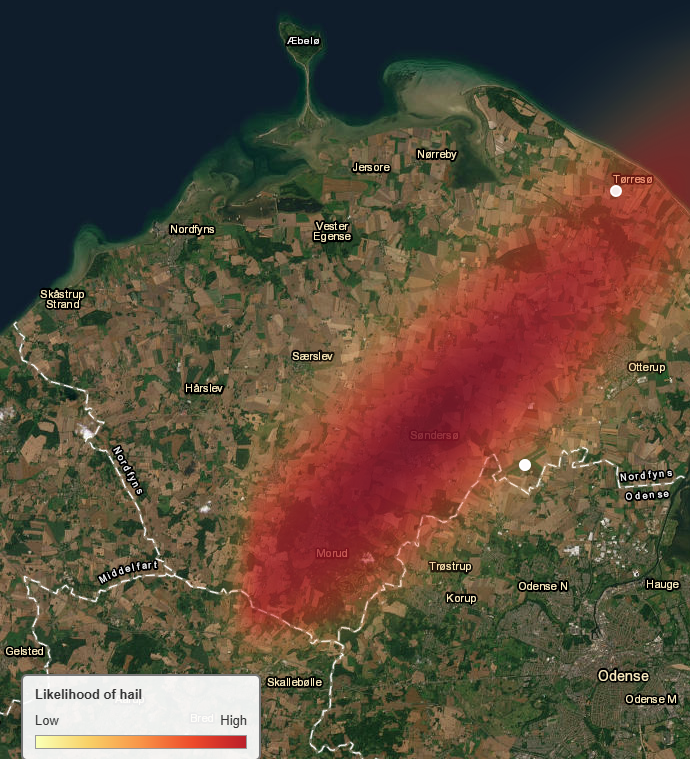

A more advanced approach is emerging through the integration of satellite data, radar observations, and agronomic analysis. By combining these sources, it becomes possible to document both the occurrence of hail and its impact on crops with far greater precision.

Meteorological radar provides insight into when and where convective storms occurred, including the likelihood of hail formation. At the same time, satellite observations allow for continuous monitoring of crop conditions before and after the event, even under cloud cover. When these signals are analyzed alongside data from nearby fields and contextual farm information, a consistent and verifiable picture begins to form.

The strength of this approach lies in the convergence of independent data sources, which together provide a far more reliable evidence base than traditional methods.

From event detection to financial impact

Confirming that hail occurred is only part of the equation. The financial impact depends on how significantly yields are affected.

A structured methodology addresses this by first estimating the expected yield in the absence of damage, based on pre-event crop development and comparable fields. It then assesses the actual expected yield following the event by analyzing post-event growth patterns and agronomic conditions. The difference between these two estimates is translated into both percentage loss and yield reduction.

By tracking crop development over time, this approach also accounts for recovery effects and seasonal dynamics. Results are typically presented with a defined uncertainty range, reflecting the natural variability in both data and modelling.

Streamlining insurance workflows

For insurers, this data-driven approach enables a more efficient and scalable claims process. Standardized assessments reduce reliance on manual inspections while improving consistency across cases.

This leads to faster claims handling and a more uniform basis for decision-making. At the same time, the quality of documentation is strengthened, which is critical in interactions with policyholders and in the event of disputes.

Automation at this level allows insurers to manage increasing claim volumes without a corresponding rise in operational complexity.

Transparency and trust

Transparency is a key advantage of a data-driven framework. When assessments are grounded in observable data and clearly defined methodologies, the rationale behind each outcome becomes easier to understand.

Access to visual evidence, time series of crop development, and structured explanations fosters greater trust between all parties involved. This reduces ambiguity and supports a smoother claims process.

A shifting risk landscape

Climate-related risks are becoming an increasingly material factor in financial portfolios. Hail is a prime example of a localized and complex hazard that is difficult to capture using conventional methods.

In this context, data-driven solutions are not merely a matter of efficiency—they are becoming essential. They enable insurers to better understand risk exposure and respond more accurately to weather-related losses.

Conclusion

Hail damage highlights the limitations of manual and subjective assessment methods. When decisions are based on sparse data, uncertainty is inevitable for both farmers and insurers.

By leveraging satellite and radar data within a standardized framework, hail damage assessment can become more objective, scalable, and transparent. This creates a stronger foundation for decision-making and supports a more effective response to climate-related risks in the insurance sector.

%20(1).jpg)

.webp)

.webp)